OUR INVESTMENT PHILOSOPHY

The cornerstone of Reams’ investment process is our predisposition toward bond market volatility. We believe market volatility is generally underappreciated and, consequently, underpriced. With this view in mind, we strive to construct portfolios that will not only withstand, but also benefit from, periods of higher market volatility.

Based on this belief, the following principles summarize our approach:

Definition of Risk: Many fixed income managers define risk as tracking error versus a benchmark. Reams defines risk as permanent loss of principal or the inability to meet investment objectives.

Predisposition Toward Volatility: Reams believes fixed income markets are inherently volatile from both an interest rate and credit perspective and, as a result, strives to construct portfolios that will not only withstand, but also benefit from, periods of higher market volatility.

Yield vs Total Return: Many fixed income managers build portfolios for yield and maintain active risk positions at all times. In periods of low interest rates and low volatility, this approach can be successful. However, a “reach” for yield (by going lower in quality or in a bond’s capital structure, for example) introduces risk to the portfolio that is likely to be magnified during volatile markets. In contrast, Reams takes a total-return viewpoint, striving to construct portfolios that perform well in dynamic environments.

Active vs Reactive: During periods of low market volatility, Reams portfolios are likely to have a higher level of liquidity, when compared to other managers, as the investment team patiently waits for opportunities to surface and then react. Reams believes this reactionary discipline is unique among bond managers and has been a distinct driver of performance.

Downside Risk Protection: Emphasis on down-side risk protection is a key to identifying securities that will perform well in volatile market conditions. This guides Reams to invest in the most senior positions of a bond’s capital structure and focus on underlying asset value. This minimizes the temptation to reach for yield by investing in lower levels of the capital structure which have significant downside risks.

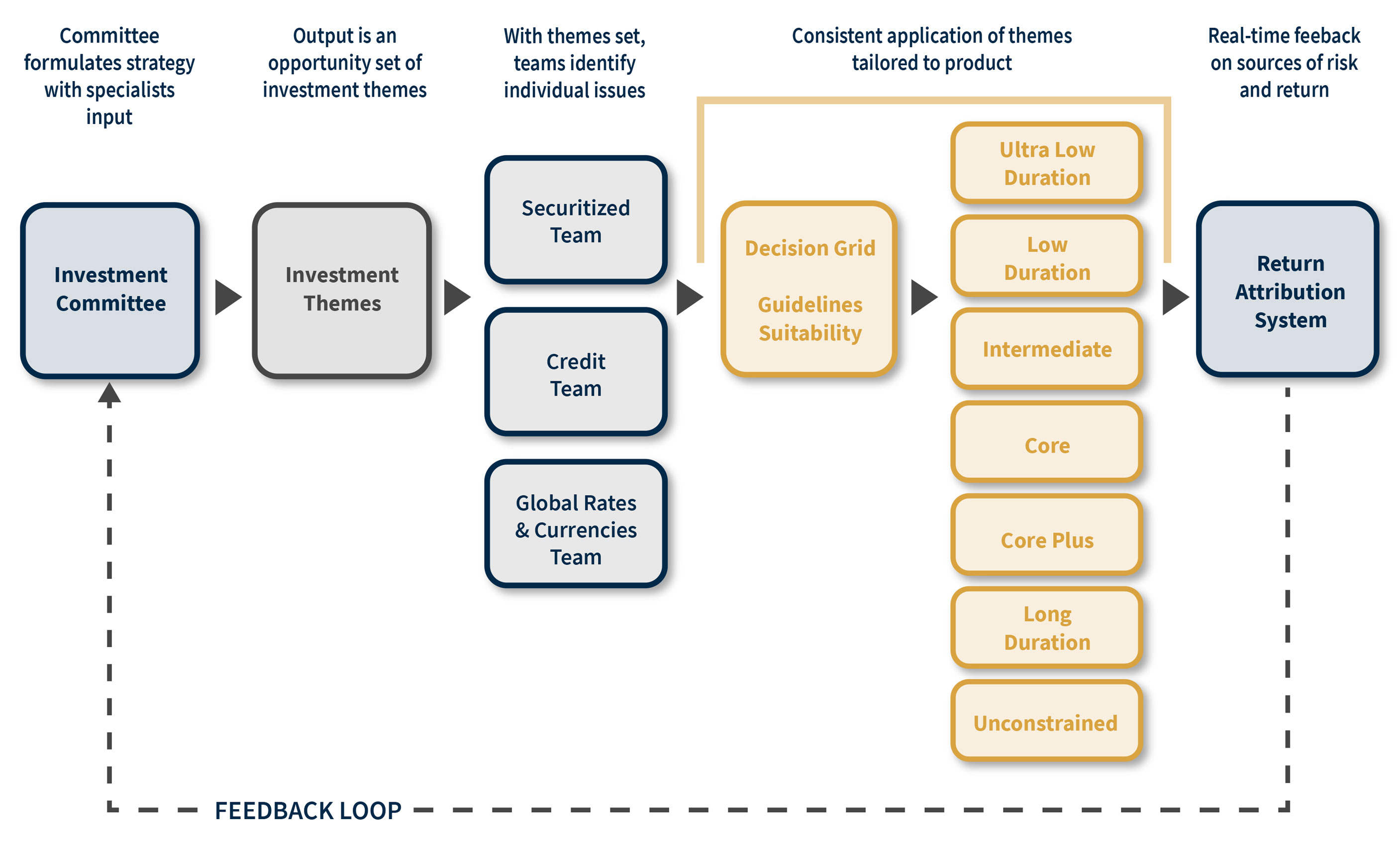

OUR INVESTMENT PROCESS

Reams manages fixed income portfolios using three basic steps, which are best described as a combination of top-down and bottom-up. The first step is the duration decision, which is based on a model in which current inflation-adjusted interest rates are evaluated relative to historical norms. With this step, the portfolio’s overall duration and yield curve characteristics are established.

The second step of the investment process is to consider sector exposures. A bottom-up issue selection process is the major determinant of sector exposure, as the availability of attractive securities in each sector determines their underweighting or overweighting in the portfolio subject to sector exposure constraints. However, for the more generic parts of the portfolio, such as agency notes and mortgage pass-throughs, top-down considerations will drive the sector allocation process on the basis of overall measurements of sector value such as yield spreads or price levels.

The third step in the investment process is individual security selection. Bottom-up issue selection is based on a scenario analysis to identify which bonds might perform best under possible interest rate and credit scenarios. The investment team then compares investment opportunities and the portfolio is assembled from the best values.

INVESTMENT PROCESS OVERVIEW